Wisconsin farms will often have many different enterprises that contribute to their whole farm business. For example, a dairy farm may have enterprises for milk sales, calf or finished cattle sales, grain sales, and hay sales. It is important for farmers to understand the income and expenses associated with each enterprise, how equipment or other […]

Farmers can use multiple tools and methods for analyzing their farm financial statements. Some are very involved and take lots of time, while others don’t take much time at all. Benchmarking is making comparisons to assist the farmer with making the best financial management decisions for their farm business that will improve financial position and […]

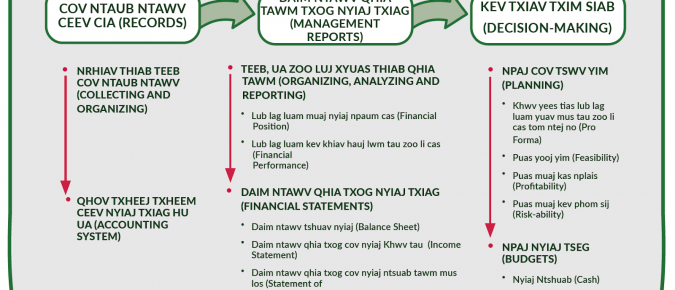

Farm financial statements, such as the balance sheet, income statement, statement of cash flows, and statement of owner equity provide a historical review of the farm business’s financial position and performance. This financial analysis provides a basis from which to plan for the future of the farm business and draft pro forma financial statements. What […]

Daim qauv ntawm daim ntawv nyiaj txiag ntawm daim teb farm financial model muaj ib qho txheej txheem hu ua linear thiab circular process kom paub qhia txog kev txiav txim siab. Cov ntaub ntawv keeb kwm no qhia mus rau daim ntawv qhia tawm (reports), thiab daim ntawv qhia tawm (reports) no pab cov tswv teb kom paub siv nyiaj thiab paub txiav txim siab txog kev ua lag luam hauv daim teb.

The second measure of financial position is solvency. Solvency is the ability of a farm business to pay all its farm debts if the business was sold tomorrow. Solvency is important in evaluating the financial risk and borrowing capacity of the farm business. Debt-to-Asset Ratio The Debt-to-Asset ratio compares a farm’s total assets with total […]

The first measure of financial performance is profitability. Profitability is the difference between the value of farm goods produced and the cost of the resources used in the production of those farm goods. In other words, profitability is what’s left after the farm business has paid all of its bills. Profitability measures the financial performance […]

The second measure of financial performance is repayment and replacement capacity. Repayment capacity shows the farm’s ability to repay term debts on time and as they come due. It includes non-farm income so it is not a measure of the farm business performance alone. The two measures used to assess repayment and replacement capacity are […]

The final measure of financial performance is financial efficiency. Financial efficiency shows how efficiently a farm business uses assets to generate income. It also indicates where each dollar of income generated in the farm business has been spent. The four measures used to assess financial efficiency are operating expense ratio, interest expense ratio, depreciation and […]

The first measure of financial position is liquidity. Liquidity is the ability of a farm business to meet the financial obligations as they come due – to generate enough cash to pay family living expenses and taxes and make debt payments on time. The two measures used to assess liquidity are current ratio and working […]

A farm business that has collected and organized their farm records will be able to complete management reports or financial statements. The Farm Financial Standards Council (FFSC – https://ffsc.org/) recommends farmers create four financial statements from which the financial position and performance may be analyzed. These statements include the balance sheet, income statement, statement of […]

Having financial statements (balance sheets and income statements) is a first step towards financial management decision-making. However, it is the next step that makes a difference in future profitability and that is analyzing the financial story being told by the financial statements and making decisions on where to spend management time to improve future profitability.

Having financial statements (balance sheets and income statements) is a first step towards financial management decision-making. However, it is the next step that makes a difference in future profitability and that is analyzing the financial story being told by the financial statements and making decisions on where to spend management time to improve future profitability.

Dairy farmers have experienced strong prices this last year, though rising input costs may have tightened cash flows. Hopefully, dairy operations are entering this new year with a strong working capital position and have adequate liquid assets available in the short term.

The new year often brings thoughts of income taxes and tax preparation. Some farmers might have received a loan servicing assistance payment if they were experiencing certain types of financial distress.

Pick up any farm magazine or listen to any farm podcast and it won’t be long before the phrase “Costs of Production” comes up. Knowing costs of production is an important piece of management information and vital in many farm management decisions. Yet, as obvious as it sounds, pop open the hood and the messiness is revealed.

Join Kevin Bernhardt, Extension Farm Management Specialist, and Katie Wantoch, Extension Farm Management Outreach Specialist, as they share financial tools and analysis methods to aid in answering these questions and making informed decisions.

Whether it is marketing decisions, best production practices, human resource management or technology adoption, a major piece of information for the farm business decision-maker is knowing the costs of production. Two major questions in determining costs of production are how to calculate and which cost of production.

There are many tools farm managers can use to inform their decision-making. One simple and effective tool for many farm management applications is breakeven costs of production. This is particularly useful in marketing decisions as the breakeven cost of production is the price needed to cover costs. If a profit goal is added to the breakeven cost of production, then the decision-maker knows what price will not only cover costs, but also a profit goal.