This article was originally published in Progressive Dairy

Benjamin Franklin famously stated, “the only two certainties in life are death and taxes.” WIth apologies to Benjamin Franklin, dairy farmers can add cyclical highs and lows in milk prices and profitability to that list.

Cyclical lows tend to be a time of greater anxiety for many and include increased exit from the industry. However, even in cyclical lows, some farms are making profits. For these farms, it is also a time of opportunity as capital asset prices for machinery, land, and cows are often lower as well. The question is: What do these successful farms look like at the end of cyclical highs that enable them to continue that success during cyclical lows?

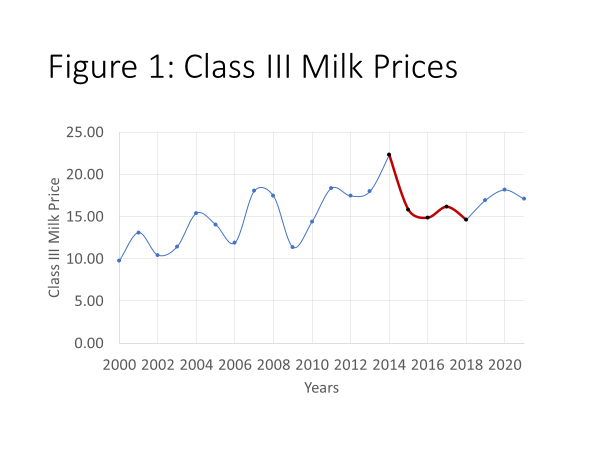

To gain insight on this question, approximately 180 Wisconsin dairy farms were assessed for the years 2014-2018 (red shaded section in Figure 1).

Year 2014 was the end of a cyclical high, followed by four years of cyclical low prices and profitability ending in 2018.

A “high-profit group” was identified based on the top 25% return on assets (ROA) in 2018 Table 1. These farms had the highest profit at the end of the four years of low prices.

All others are referred to as the “low-profit group”. The assumption was that farms with the highest profitability coming out of a low in the profit cycle did something right during the high in the cycle to prepare their operation. What did the high profit group look like at the end of 2014 that prepared them for continued success in the low years that followed?

Virtually everyone made money in the cyclical high year of 2014. Of the 180 farms studied, 171, or 96%, had positive ROA in 2014. However, only 86 (48%) had positive returns in 2018. So the question is: What was significantly different between the high- and low-profit groups coming out of the high year of 2014? Was it the amount of debt, working capital, price, costs of production, or herd size, or a little of all of the above?

Note, “significant” has a special meaning in statistics. It means that after considering the number of observations, average, and variation around the average it can be said with confidence that the averages are different. Table 1 shows the results. Statistical difference is measured by the “P-Value” in Table 1. If the P-Value is less than .05, then there is 95% confidence that the high- and low-profit groups are different (these are noted in Table 1 with a double asterisk). P-Values from .051 to .100 mean there is 90% confidence (noted by a single asterisk).

What was different?

While virtually all 180 farms were profitable in the cyclical-high year of 2014, the high-profit group was significantly more profitable, with a ROA of 9.0% versus 6.5% for the low-profit group. The additional profitability perhaps provided the tailwind going into the low years. More importantly, what made them more profitable?

Return on Assets comes from two primary sources. The first is the ability to create revenues from assets (measured by the asset turnover ratio). That is, how well is the farm doing in creating gross revenues from cows, tractors, land, and other assets. Second is being efficient with expenses (measured by the operating profit margin ratio). That is, how well did the farm do at keeping revenues (net income) after all the expenses were paid?

In 2014, the asset turnover ratio was not different, indicating that both groups knew how to work their assets (cows, land, etc.) to create gross revenues. However, the operating profit margin ratio was significantly different, indicating that high profit farms were more efficient with their expenses.

Efficiency can come from producing the same amount of product but at a lower cost, producing more product at the same cost, or both. Production per cow was significantly higher for the high-profit group (+1,350 more pounds per cow per year). This difference, itself, is not staggering (13.5 cwt for the entire year or about 4.4 lbs per cow per day for a 305-day lactation). However, in addition to a bit more milk to sell per cow, the high-profit farms produced the extra milk with the same or lower costs of production per hundredweight equivalent (cwteq ). Operating expenses, including depreciation and labor costs, were $1.26 less per for the high-profit farms.

For perspective, a 200-cow dairy from the high-profit group had additional production per cow (13.5 cwt) and slightly lower cost of production per cwteq ($1.26). Using the average 2014 price for all farms ($24.39 cwt), then this farm generates +$71,063 more net income for that year.

Another source of profitability is price. However, price was not significantly different between the two groups. This is not a surprise, as all farms in this study were commodity farms and therefore price takers. Price differences can result from discounts, premiums and marketing, but those were not enough overall to create a difference in prices between the two groups.

Whether measured in total assets, herd size, or acres owned, farm size was significantly greater for high-profit farms. This group owned $1.9 million more assets, 129 more cows, and 88 more acres as compared to the low-profit farms. However, assets per cow was slightly less for the high-profit farms, and depreciation costs per cwteq was $.28 less for this group.

What was not different?

Farm managers, lenders, and consultants often focus on the need to keep debt at a moderate level and maintain good working capital. These are sound risk management strategies, but not as obvious when it comes to profits. No matter how it was measured, the level of debt and working capital was not different between high- and low-profit farms. In-fact, the high-profit farms had more debt per cow, more debt per cwteq, a higher debt to asset ratio, but the same level of working capital. Statistically, the two groups were not different.

That said, the key was how the debt was used between these groups. If debt is used to purchase assets, make improvements, or improve processes, that results in a 10% return on profits on that debt. If the interest rate on the debt is 6%, then the additional 4% is net profit that goes in the owner’s pocket. In this scenario, the return on borrowed capital is greater than the interest rate paid for it. This is sometimes referred to as an equity multiplier.

However, the reverse is true as well. If the return on debt is 6% and the interest rate is 10%, then the farm business has to come up with the other 4% from somewhere else in the operation. The equity multiplier is still working, it’s just negative!

Whether debt is being used to leverage greater profitability, or is a drag on profitability, can be measured by whether return on equity (ROE) is greater than return on assets (ROA).

Coming out of the cyclical-high year of 2014, 73% and 56% of high- and low-profit farms, respectively, had a ROE greater than ROA. That means debt was being used on these farms to leverage greater profitability, but more so for the high-profit farms. However, after prices fell, it was much harder to have profit returns greater than the interest paid. In 2018, after four years of low prices, 42% of high-profit farms still were leveraging debt for higher returns, but only 4% of low-profit farms had the same. This indicates that while the level of debt was not different, how debt was managed and used may be a unique difference for those farms able to maintain profitability even in cyclical-low priced years.

Working capital is the equation of current assets less current liabilities. It is a measure of the capacity to absorb any risks that may occur, including profit losses, take advantage of opportunities that arise, and for normally occurring transactions. Common wisdom is to maintain a high level of working capital. However, working capital also has an opportunity cost. It could be used to pay off debt, especially debt that is not returning a profit greater than the interest paid for it, or could also buy revenue-generating assets, both of which potentially could add profitability.

How do you balance this? A business wants enough working capital to accommodate risk and opportunity, yet not so much that it is losing too much on opportunity costs. If a farm business has done well at mitigating potential risks and perhaps has a largely unused line of credit, the business could likely have less working capital while still maintaining enough for risk, opportunity, and normal transactions.

Did high-profit farms take advantage of opportunities?

When milk prices are depressed, prices of capital assets such as cows, land, machinery, etc., sometimes level out or even fall. Thus, for those businesses that have dollars to invest, there may be opportunities. While all farms on average grew in cows, acres and total asset value, the high-profit group grew faster during the cyclical low years by .8%, 19.5%, and 4.0% respectively, for herd size, acres owned and total assets.

Research results often confirm the common sense we already knew. Results indicate that the farms that not only survive but thrive and grow during cyclical lows are those that run a tight ship. Their management results in slightly greater cost efficiencies and slightly higher production. However, taken together, the impact is significant. Further, they manage debt in ways that return greater profits than the interest they pay. As a result, they can take advantage of opportunities and grow the business.

What does it all mean for what to do tomorrow after breakfast to prepare for the next cyclical low?

- Are there new practices, protocols, negotiations, or technology that will

- increase cost efficiencies in feeding, health, breeding, transition, and replacements without decreasing production;

- increase production without decreasing cost efficiencies;

- or both?

- Is there debt that is not pulling its weight with respect to earning more profits than the interest being paid for it?

- If so, can a plan be put in place to pay it off quickly? As interest rates increase, loans under variable rate may trip over into a profit-reducing situation.

- Is there new debt financing that would improve production, increase cost efficiencies, or both that has the potential of a much greater return than the interest paid?

- Are there enterprises, practices, technology that are fine today when there are high prices, but would be a drag on profitability if prices fall and/or interest rates and costs increase? The high of the profit cycle may be the time to make the change.

- Are there investments being considered at the high of the price cycle when there is lots of cash, that are affordable today, but would quickly become problematic if prices fall and/or interest rates and costs increase? Maybe this is the time to say “no” to this situation.

It may seem counterintuitive, but perhaps the best time to focus on running a tight ship is during the good times so that the business is ready to capitalize during cyclical lows.

1 cwteq = Hundredweight Equivalent. Hundredweight equivalent is a means to adjust costs of production per sales unit to just the primary product, in this case, milk. The cwteq is total farm income divided by milk price. Dividing costs by the cwteq is more reflective of the cost of producing just milk versus charging the cows for corn and other enterprise production costs.

Table 1: Farm characteristics and significance tests of high versus low profit groups

| 2014 (Cyclical High) | 2018 (Cyclical Low) | |||||

| High Profit | Low Profit | P-Value1 | High Profit | Low Profit | P-Value1 | |

| Number of farms (N) | 45 | 133 | 45 | 133 | ||

| Return on Assets (ROA), % | 9.0 | 6.5 | .005** | 5.0 | -1.7 | .000** |

| Return on Equity (ROE), % | 11.9 | 8.7 | .026** | 5.9 | -9.5 | .000** |

| Price, $/cwt | 24.47 | 24.31 | .268 | 17.40 | 16.60 | .046** |

| Production, lbs/cow/year | 23,678 | 22,328 | .052* | 24,344 | 22,467 | .010** |

| Operating COP2, $/cwteq3 | 13.80 | 14.54 | .070* | 10.00 | 12.16 | .000** |

| Depreciation COP, $/cwteq | 1.95 | 2.23 | .051* | 1.66 | 2.01 | .008** |

| Interest COP, $/cwteq | .67 | .68 | .477 | .68 | .84 | .043** |

| Labor COP, $/cwteq | 3.16 | 3.40 | .090* | 2.62 | 3.28 | .000** |

| Non-Milk Revenue:TR4 | 20.3% | 17.0% | .067* | 22.7% | 17.0% | .020** |

| Total Assets, mil. | 5.723 | 3.788 | .007** | 6.291 | 4.012 | .007** |

| Total Liabilities, mil. | 1.755 | 1.191 | .046** | 2.078 | 1.698 | .181 |

| Debt to Asset Ratio, % | 27.9 | 25.6 | .229 | 30.4% | 32.7% | .270 |

| Debt per Cow | 4,816 | 4,383 | .203 | 5,246 | 5,298 | .469 |

| Debt per cwteq | 16.39 | 16.34 | .489 | 15.34 | 18.79 | .042** |

| Herd Size, head cows | 361 | 232 | .015** | 423 | 270 | .017** |

| Acres Owned | 359 | 271 | .047** | 449 | 286 | .003** |

| Working Capital to TR, % | 25.6% | 25.8% | .482 | 24.9% | 28.4% | .172 |

| Operating Profit Margin, % | 20.9 | 16.1 | .008** | 14.3 | -6.4 | .000** |

| Asset Turnover Ratio, % | 43.6% | 39.1% | .116 | 35.6% | 28.4% | .011** |

| Operating Expense Ratio, % | 69.1% | 70.1% | .302 | 73.9% | 82.6% | .000** |

| Depreciation Expense Ratio | 8.1% | 9.2% | .050* | 10.3% | 12.5% | .008** |

| Interest Expense Ratio, % | 2.8% | 2.8% | .477 | 4.2% | 5.3% | .043** |

1 P-Value is a measure of statistical difference. Values from zero to .05 mean there is 95% confidence that the High and Low profit group are different. Values from .051 to .10 mean there is 90% confidence that the High and Low profit group values are different.

2 COP = Cost of Production before depreciation, interest, and labor.

3 cwteq = hundredweight qquivalent. Hundredweight equivalent is a means to adjust costs of production per sales unit to just the primary product, in this case, milk. The cwteq is total farm income divided by milk price. Dividing costs by the cwteq is more reflective of the cost of producing just milk versus charging the cows for corn and other enterprise production costs.

4 TR = Total Revenue from all sources.