“Is my operation big enough?” It’s a loaded question that includes values, policy, lots of opinions, more than a few arguments, and even a little economics, the latter of which is the subject here. Economically “big enough” is the capacity needed to achieve profit goals given prices and costs of production.

There are two sources of capacity – production efficiency and scale.

- Production efficiency is how many sales units are produced per production unit (bushels per acre, hundredweights per cow, or pounds per tree).

- Scale is the total number of production units (acres, cows, or trees).

One may grow corn over half the county, but if production efficiency is low (bushels per acre), then there may be a capacity challenge. That is, more acres will not help profitability if the bushels per acre are too low to cover costs per acre. Alternatively, one may be extremely efficient at producing bushels per acre of corn, but if there is only fifty acres, then capacity (scale) may not be enough to cover total income needs.

Capacity is also dependent on the business model. A commodity corn producer may need 1,000 acres or more to attain a desired net income goal, while 300 acres of organically grown corn or 25 acres of wine-making grapes may achieve the same net income.

Math of Profits

Evaluating the two sources of capacity begins with the profit equation. The math of profits is derived in more detail in appendix 1, but in simple form, profits can be expressed as:

- Profits = [(P – VC) x Q] – FC

Where: P = Price

VC = Variable costs

Q = Quantity of sales units (bushels, hundredweight, pounds)

FC = Fixed Costs

The total quantity of sales units (Q) comes from the two sources of capacity, that is, the total number of production units (acres, cows, and trees) and how much each is producing (bushels per acre, hundredweight per cow, or pounds per tree). Thus, total sales units (Q) can be expressed as:

- Q = (Q/q) x (q)

Where: q = Quantity of production units (acres, cows, or trees)

Substituting Equation 2 into Equation 1 gives:

- Profits = [(P – VC) x (Q/q) x (q)] – FC

Production efficiency (Q/q) and scale (q) are the two sources of capacity that impact profits. Profit Equation 3 provides a roadmap for management analysis and decision-making. However, let’s put Equation 3 into an easier to understand context of milk and corn production.

- (3a) Total Milk Profit = [(milk price – VC) x (cwt/cow) x (cows)] – FC

- (3b) Total Corn Profit = [(corn price – VC) x (bu/acre) x (acres)] – FC

The profit equations for milk and corn (3a and 3b) show the four components of profits, two of which are the sources of capacity.

- Profit margin per unit of production, (milk price – VC) or (corn price – VC), which can improve profits by:

- Increasing price through marketing, premiums, discounts, etc.

- Reducing variable costs through best practices, bulk purchasing, timing discounts, labor management, etc.

- Or both.

- Capacity via production efficiency, (cwt/cow) or (bu/acre), which can improve profits by:

- increasing sales units produced per production unit through better nutrition, timeliness, genetics, etc.

- Capacity via scale (total number of cows or acres), which can improve profits by:

- increasing the total number of production units and potentially lowering fixed costs in the long run.

- Fixed costs (FC).

- Fixed costs cannot be changed in the short run, but they can be reduced in the long run and one major way to do so is through economies of scale (capacity).

Analysis of how to improve profitability becomes an analysis of these four different areas and decisions on how one or more can be improved. However, an important reminder is that the profit equation is dynamic. That is, a farm manager can change practices to increase production per cow by using higher quality feeds, more veterinary care, better genetics, or improved cow comfort. However, these changes may also increase costs. Thus, it becomes a question of proportionality, that is, can production be increased by relatively more than the increase in costs.

Similarly, scale can be increased to create economies of scale (lower fixed costs), but there may also be impacts on variable costs, production per unit, and even price. The impacts may be positive or negative depending on how the increase in scale is managed.

Capacity and Breakeven Analysis Tool (Capacity tab)

The “Capacity and Breakeven Analysis Tool” spreadsheet enables analysis of capacity questions given a business model and its accompanying prices, costs, and profit goals. The tool can be used to analyze the “how big” question, that is, how many acres, cows, or trees are needed to achieve a user defined profit goal based on various combinations of prices and costs of production.

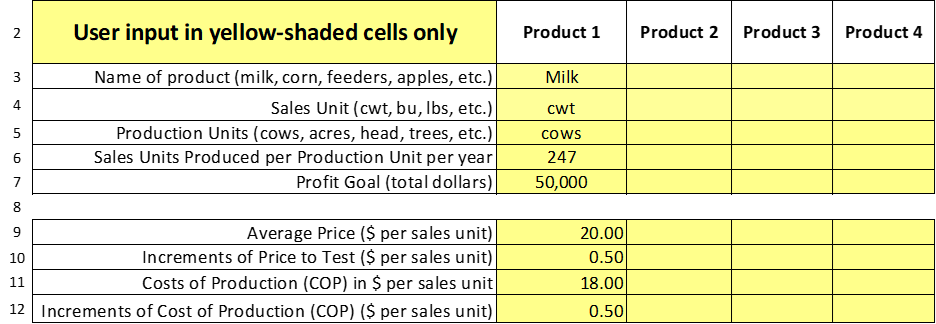

Beginning with the ‘Capacity’ tab, the user defines the product being analyzed, sales units, production units, prices, costs of production, etc. Table 1 shows an example from the spreadsheet. Up to four products can be analyzed (only Product 1 for milk is shown in this example). For the milk example, sales units are hundredweight (cwt), production units are cows, each cow produces on average 247 hundredweight of milk per year (24,700 pounds), and the profit goal is $50,000.

The next block of entries in rows 9-12 is information on prices and costs of production to use in the analysis. The example shows an expected average price of $20.00 (line 9), costs of production of $18.00 (line 11), and $.50 increments both lower and higher around price and costs of production (lines 10 and 12). The increments will provide a range of results (sensitivity analysis). For this example, the increments lower and higher are set at $.50 for both price and costs of production, however, they do not have to be the same. Also note, that the costs of production ($18.00 in this example) are total costs including both variable and fixed.

Table 2 shows the results. Based on a price of $20.00 and costs of production of $18.00 ($2.00 per hundredweight profit margin), it would take 101 cows of capacity to achieve the $50,000 profit goal. Note, the table also shows results for a range of prices and costs of production based on the $.50 increments entered in Table 1. If price increases to $21.00 and costs remain at $18.00 ($3.00 profit margin) then it would take capacity of 67 cows to achieve the profit goal. However, if price falls to $19.00 and costs remain at $18.00 ($1.00 profit margin), then it would take 202 cows.

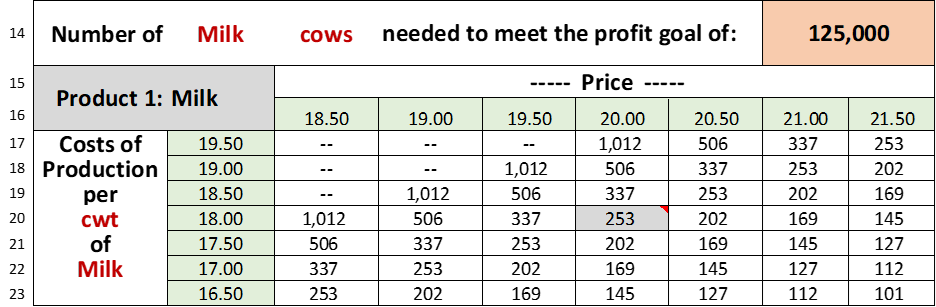

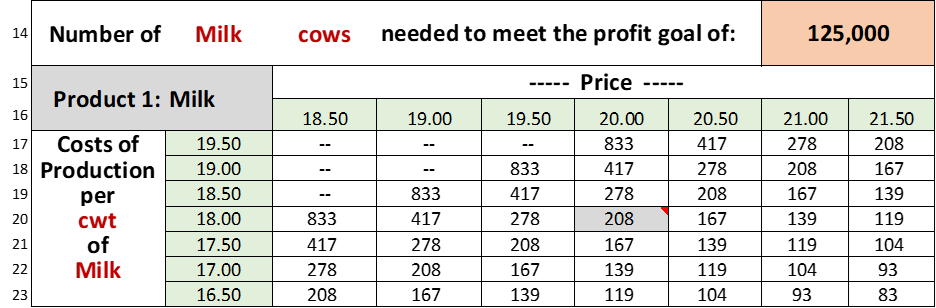

Table 3 shows what happens to capacity needs if all entries remain the same except the profit goal which is increased to $125,000. Now, the same $20.00 milk and $18.00 costs of production requires a capacity of 253 cows to meet the higher profit goal.

Finally, Table 4 shows what happens if all prices, costs of production, and the profit goal remain the same ($20.00, $18.00, and $125,000 respectively), but the production per cow is increased to 30,000 pounds per cow or 300 hundredweights versus the current 247. The number of cows needed to achieve the $125,000 profit goal is now 208 cows versus 253 cows when production efficiency was lower.

The spreadsheet is easy to use, but caution is needed to remember that the spreadsheet is static while real life is dynamic. That is, using the example shown in Table 4 of increasing production per cow from 24,700 pounds per year to 30,000 pounds per year likely comes with changes in costs of production to achieve that increase.

Capacity and Breakeven Analysis Tool (Breakeven Price tab)

The ‘Breakeven Price’ tab is like the ‘Capacity’ tab except that the results are in terms of the price needed instead of capacity to cover costs of production and profit goals. In this tab, the user defines total costs of production, total production, and profit goal. Note, that a true breakeven price is where the profit goal is set to zero.

Table 5 shows results of a situation where there are 200 cows producing 24,700 pounds of milk per cow or 49,400 hundredweights of milk for the herd. Total costs of production are $18.00 per hundredweight for a total of $889,200 and the profit goal is set at $150,000.

Based on the user entered information, it would take a price of $21.04 to cover the $889,200 of total costs and profit goal of $150,000 given total production of 49,400 hundredweights. As was the case with capacity, some sensitivity analysis is included to test ranges of costs and production lower and higher than the given values. In this case the sensitivity is based on percentage higher and lower, where the percentage is defined and entered by the user.

The debate on farm size has values, policy, and political dimensions. However, for the farm business manager farm size, or capacity, often becomes an economic question that is unique to their situation and their business model. Bigger is not better and bigger is not worse, it all depends. It depends on the type of farm, business model, current physical infrastructure, cost structures, transition situation, family lifestyle, management skill sets, and much more. No matter the situation, there is an optimal capacity that achieves the goals of the farm given prices, costs, and profit goals. Likewise improving profitability is a dynamic interplay between prices, costs, and capacity. Understanding the math of profits is a good place to start.

Table 1: User Information for Determining Capacity

Table 2: Results of Capacity Needed for the Milk Product Example Shown in Table 1

Table 3: Results of Capacity Needed for a Profit Goal of $125,000

Table 4: Results of Capacity Needed for Production per Cow Increase to 300 cwt/cow

Table 5: Breakeven Price Needed to Cover Costs and Profit Goal Given Levels of Production

Appendix 1

Math of Profits

The profit equation in its simplest form is:

- Profit = Total Revenues (TR) – Total Costs of Production (COP)

Total revenues (TR) are a product of a constant standardized price per unit of sales (P)2 times total sales units sold (Q). Substituting into (1) gives:

- Profit – (P x Q ) – COP

Total costs of production (COP) include total variable costs (TVC) and fixed costs (FC). Total variable costs change with the number of intended sales units produced while fixed costs in the short run are a constant regardless of intended production. Note, in the long run, all costs are variable. Total variable costs can be expressed as a standardized variable costs per sales unit (VC) times the number of sales units (Q). Thus COP = (VC x Q) + FC. Substituting into (2) for COP gives:

- Profit = (P x Q) – (VC x Q) – FC

Collecting terms, (3) can be rewritten as:

- Profit = [(P – VC) x Q] – FC

Total sales units produced (Q) such as bushels, hundredweights, or pounds comes from the production efficiency of the number of sales units produced per production unit (bushels per acre, hundredweights per cow, pounds per tree) times scale (q) such as acres, cows, or trees. Thus, the variable (Q) in equation (4) can be rewritten as:

- Q = (Q/q) x (q) where “q” is production unites (acres, cows, trees)

Substituting (5) into (4) for gives:

- Profit = [(P – VC) x (Q/q) x (q)] – FC

The math of profits in the form of equation (6) shows the building blocks for total profits:

- Profit margin per unit of sales (P – VC).

- Capacity via production efficiency (Q/q).

- Capacity via total production units or scale (q).

- Fixed costs (FC).

1 Kevin Bernhardt is a Farm Management Outreach Specialist with the UW-Madison Division of Extension and Professor of Agribusiness at University of Wisconsin Platteville.

2 One might want to express price per unit of sales as P/Q, after all, if follows the words used. However, price (P) is a unit price that is already a standardized and constant value that does not change with quantity. Total revenue changes with quantity, but not the standardized unit price. More elaborate forms of the profit equation can have price as a function of quantity, which would allow price to vary with total sales quantities. That does not change the overall component sources of profits but does give another place where capacity has an impact.